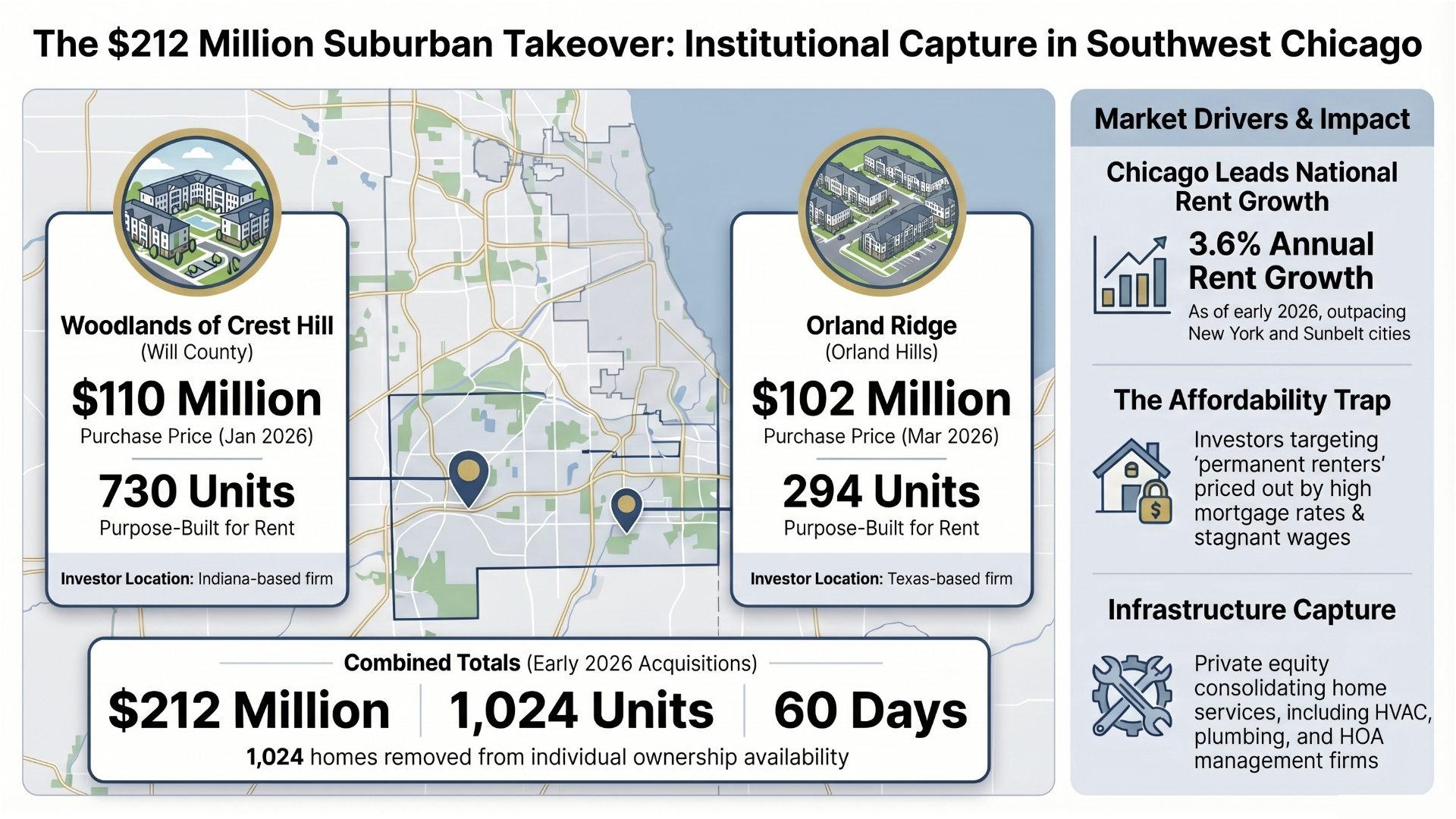

In January 2026, an Indiana-based investment firm paid $110 million for 730 rental units in Crest Hill, Will County. Two months later, a Texas-based company paid $102 million for 294 rental units in Orland Park. Together: $212 million, 1,024 homes, none of them for sale, all within about 35 miles of downtown Chicago. These are not scattered rentals picked up by a local landlord. These are large-scale institutional acquisitions, part of a national strategy to build and own entire communities designed specifically so people never get the option to buy.

For a while, the story about institutional investors buying up housing was easy to dismiss if you lived here. That was a Phoenix problem. An Atlanta problem. A Charlotte problem, somewhere down South where land was cheap, growth was fast, and corporate landlords had been operating at scale for years. Not here. Not in the southwest suburbs of Chicago, where most people still buy a house, build equity, and eventually hand something down to their kids.

That story just got harder to tell.

Two deals closed in the first quarter of 2026 within a short drive of each other, totaling more than $212 million in institutional investment in rental housing, right here, in Will County and Cook County ,Orland Park. I want to walk through what happened, why it happened, what the business logic is, and what I actually think about it. Because I don't think this is neutral news, and I'm not going to pretend otherwise.

- Two institutional investors spent a combined $212 million acquiring 1,024 rental units in Will County and Orland in the first 60 days of 2026.

- Both deals are part of a national trend called Build-to-Rent (BTR), communities purpose-built so the homes inside are never available for individual purchase.

- The BTR model was concentrated in the Sunbelt for years. It is now expanding into Midwest suburbs, with the Chicago metro leading national rent growth at 3.6% annually.

- Private equity is simultaneously acquiring HVAC companies, plumbing companies, HOA management firms, and water utilities, capturing not just where people live, but everything that keeps a home running.

- My position: this pattern, if it continues unchecked, points toward a future where a permanent renter class is not an accident, it's the business model.

- For current homeowners in this market, equity still matters, and the decision of when and whether to sell carries more weight than it did even five years ago.

This Was Supposed to Be a Sunbelt Problem

The Build-to-Rent model isn't new. Institutional investors have been building and acquiring communities of rental single-family homes and townhomes for years, primarily in Texas, Florida, Arizona, Georgia, and the Carolinas. The pitch to investors is straightforward: build a neighborhood of homes that look like ownership housing, price them out of reach for buyers, and collect rent from a captive pool of people who want more space than an apartment but can't afford, or can't qualify for a mortgage.

For a long time, that model stayed in the Sunbelt because that's where the land was affordable enough and the population growth was fast enough to support it. Phoenix made sense. Nashville made sense. The southwest suburbs of Chicago did not seem to be next in line.

The numbers say otherwise now. Annual BTR home starts nationwide hit a record 92,000 in the third quarter of 2024, up 455% from pre-pandemic levels. There are more than 64,000 BTR units currently under construction across the country, with the pipeline extending through late 2027. More telling for this market: the Midwest led all regions in BTR rent growth in early 2025, at 4.2% year-over-year, precisely because supply here is so historically low. The Sunbelt is getting crowded. Investors are following the math north.

And according to Yardi Matrix, as of early 2026, Chicago was the top market in the country for annual rent growth, 3.6%, ahead of New York, the Twin Cities, and every major Sun Belt city. That is not the kind of number that goes unnoticed by people who move $100 million at a time.

What Just Happened Here

Two deals. Both closed in the opening months of 2026. Both targeting rental communities in markets that most people in this area would describe as normal, middle-class suburbs.

Deal One, Woodlands of Crest Hill, Will County (January 2026): Bayshore Properties, an Indiana-based investment firm, acquired the 730-unit Woodlands of Crest Hill apartment community at 1615 Arbor Lane in southwest Will County for $110 million. The financing was arranged through Greystone, using a $89 million Fannie Mae first loan and a $5.5 million second loan, both non-recourse, both structured for a 10-year hold. That last detail matters: this isn't a flip. They are planning to own and operate this property for a decade.

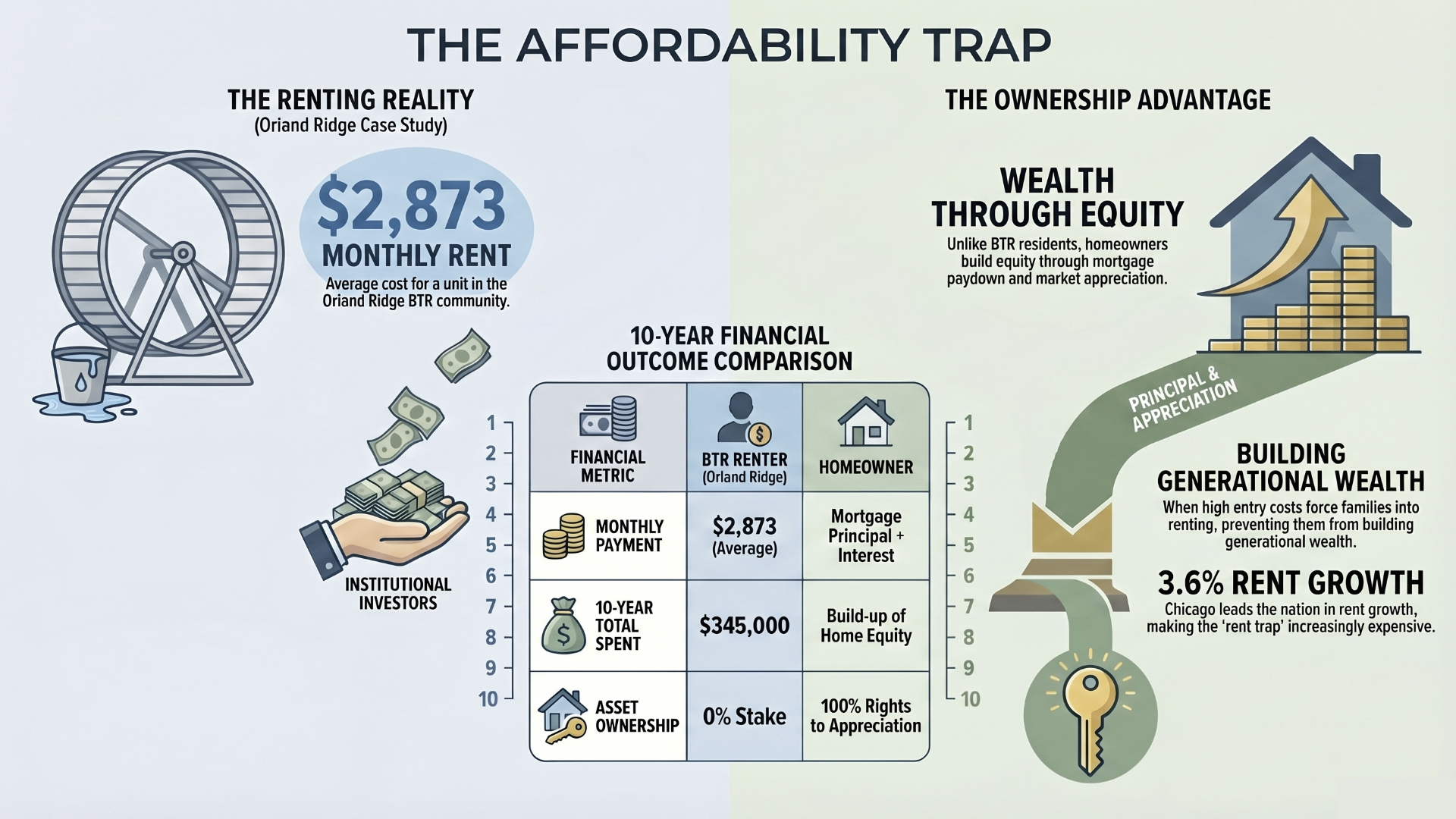

Deal Two, Orland Ridge, Orland (March 2026): RPM Living, an Austin, Texas-based investment and management company, paid $102 million for the 294-unit Orland Ridge community at 16966 Pond Willow Drive, on the corner of 171st Street and LaGrange Road, right next to the Orland Grassland and Nature Preserve. The property includes townhomes and ranch villas, averaging 1,455 square feet per unit, and was operating at 92% occupancy when the deal closed. Average rent at the time of acquisition was $2,873 per month.

Together, that is $212 million in institutional capital, 1,024 rental units, and two investors based in Indiana and Texas who just became significant players in the southwest Chicago suburb housing market. The sellers, SR Jacobson Development and Lormax Stern for Orland Ridge, and Osso Capital for Woodlands, made their exits. The buyers are staying.

The Business Logic, And Why It Works Against You

To understand why this is happening here, you have to understand what investors are actually buying.

They are not buying real estate in the traditional sense. They are buying income streams, predictable, recurring monthly revenue generated by people who need a place to live. The same logic that makes HVAC maintenance contracts attractive to private equity is what makes a 294-unit rental community attractive: the demand doesn't go away, the cash flow is largely predictable, and the customer has limited alternatives.

What makes this moment different is the affordability trap that the broader housing market has constructed over the past several years. Harvard's State of the Nation's Housing found that 22.6 million renter households in the U.S. were cost-burdened in 2023. The same report put the income needed to afford a median-priced home at around $126,700 per year, and found that only about 6 million of the country's nearly 46 million renters actually meet that threshold. The rest are priced out. Not by choice. By math.

That math is the product institutional investors are selling. High home prices plus elevated mortgage rates plus stagnant wages equals a large and growing pool of people who will rent a single-family style home indefinitely because the ownership path is effectively closed. BTR communities are designed to capture that pool, offering the square footage, the garage, the yard, and the neighborhood feel of ownership housing, at a monthly rent that keeps those residents perpetually renting rather than building equity.

At $2,873 per month at Orland Ridge, a renter there will spend roughly $34,500 per year in rent. Over ten years, that's $345,000, assuming no rent increases, which is not how any of this actually works. In that same decade, a homeowner building equity in a comparably priced property in the same area would be in an entirely different financial position. That gap is the product. The renter's financial stagnation is part of the return calculation.

It's Not Just the Roof Over Your Head

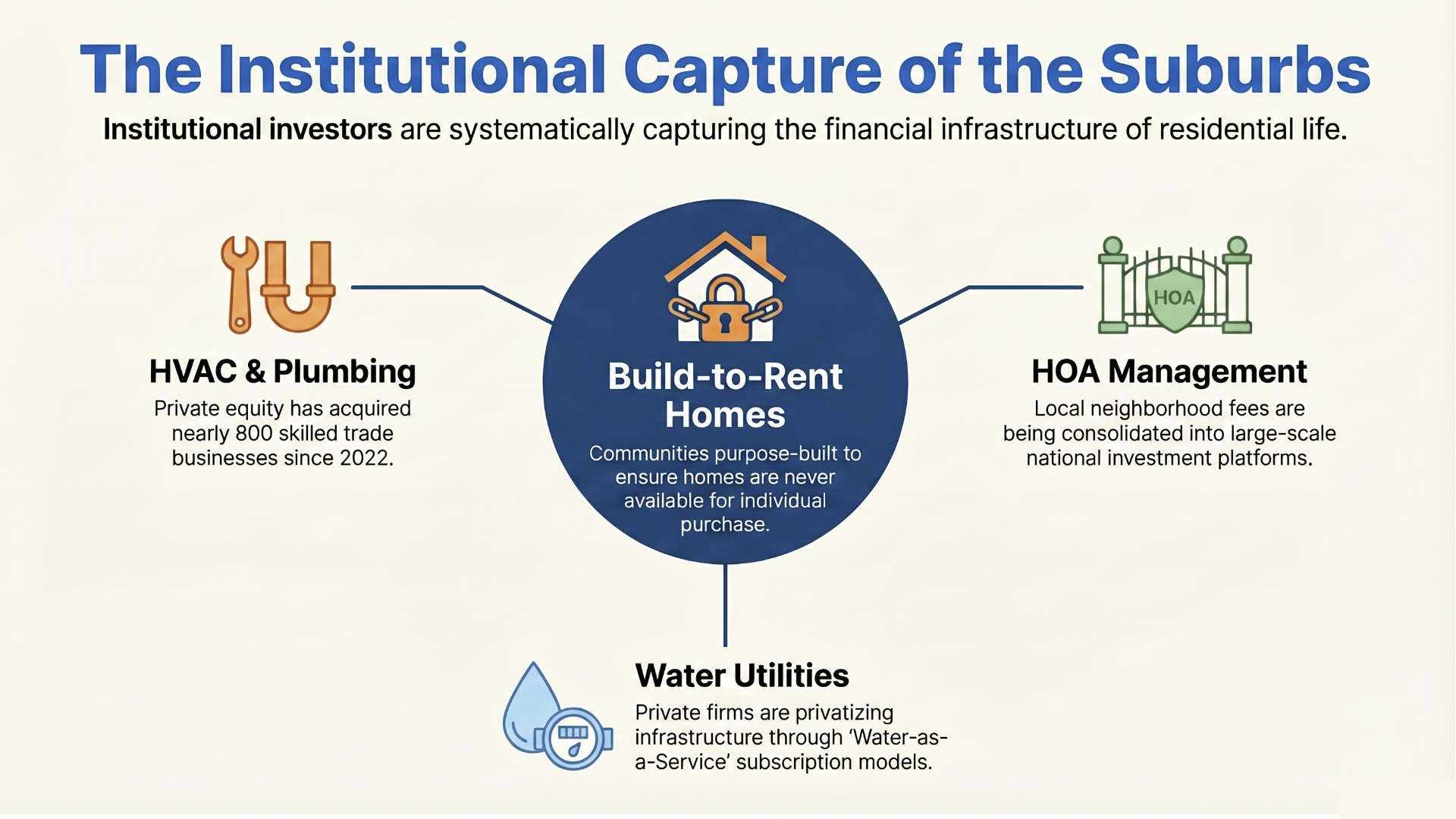

If institutional money were only buying rental communities, the story would be significant enough. But it doesn't stop there, and this is the part I want people to pay attention to, even if it sounds like a tangent.

Private equity has been quietly acquiring the companies that service the homes people live in. HVAC companies, plumbing contractors, electrical businesses, the trades that every homeowner and renter depends on when something breaks. According to the Wall Street Journal, PE firms have purchased nearly 800 skilled trade businesses since 2022 alone. 2024 was a record year for HVAC-focused acquisitions. Many of these companies keep the same local name and logo after the sale, so homeowners have no idea the family-owned business they called for 15 years is now part of a corporate portfolio operating across dozens of states.

HOA management is following the same path. There are currently about 15 private equity firms actively acquiring HOA and community association management companies, consolidating what was once a local, neighborhood-level service into large national platforms. The multi-billion dollar ecosystem of HOA fees, vendor contracts, and maintenance assessments that govern 40 million U.S. households is being treated as acquisition territory. If you live in a community with an HOA, the company managing it may already be part of a PE-backed roll-up you've never heard of.

Water utilities are also being privatized at an accelerating pace. Private equity has executed more than 435 transactions in the water sector since 2015, with active holdings more than doubling since 2019. A new subscription model called Water-as-a-Service is emerging, where municipalities and even residential communities pay for water access rather than owning the infrastructure. The U.S. accounts for 73% of active PE water holdings globally.

The pattern is not subtle: the roof, the furnace, the pipes, the HOA, the water. Each piece of the infrastructure of everyday residential life is being consolidated under institutional ownership, optimized for returns, and repriced accordingly. You don't have to own the house to control what it costs to live there.

My Take, And I'm Not Going to Pretend I Don't Have One

I've been a real estate broker in this market for more than 20 years. I've worked with buyers trying to get into their first home, sellers trying to time a move, families navigating probate and divorce, and people making the hardest financial decision of their lives. I'm not anti-investor. I'm not anti-development. And I understand that not every institutional acquisition is some conspiratorial plot against regular people.

But I also know what equity does for a family over time. I've watched homeowners in this market build real wealth, not because they got lucky, but because they owned something that appreciated, paid off a mortgage, and gave them options. That is what ownership makes possible. Renting doesn't build that. Renting, at $2,873 a month in a community designed specifically to never convert to ownership, builds nothing except someone else's return.

When I look at the pattern, purpose-built rental communities, PE buying the trades that service those homes, PE rolling up the HOAs that govern them, PE privatizing the water utilities that supply them, I don't see a neutral market correction. I see a systematic capture of the financial infrastructure of residential life. And the end state, if the trend continues without meaningful policy pushback, is a permanent renter class that is kept financially stagnant not by accident but by design.

I'm not predicting doomsday. I don't know exactly how this plays out, and I won't pretend to. But I do know that two deals totaling $212 million just closed in Orland and Will County in 60 days, and the people making those investments are not doing it for the community's benefit. They're doing it because the math works for them, and the math works for them precisely because homeownership has become harder for everyone else.

That's worth knowing. And it's worth having an opinion about.

What It Means for This Market

For current homeowners in Frankfort, Mokena, New Lenox, Tinley Park, Orland Park, Homer Glen, Lockport, and surrounding areas, a few things are worth keeping in mind.

Your equity is real and it matters now more than it did five years ago. The gap between what a homeowner accumulates over time and what a renter accumulates has widened, not narrowed, as prices have risen and institutional capital has moved into the rental side of the market. If you've been sitting on appreciated equity and waiting to make a decision, the environment around you is changing in ways that make that equity more valuable, not less.

The rental market becoming more institutionalized does not directly affect your ability to sell your home, but it does change the long-term picture for your neighborhood, your community's demographics, and the pipeline of future buyers. More institutionally owned rental communities means more of the housing stock is held off the for-sale market. That keeps supply thin and supports prices for homeowners who do sell, but it also raises questions about what the ownership landscape looks like in 10 or 20 years.

And if you are a renter right now, or you have adult children who are renting while trying to save for a home, the math is not getting easier. The institutional BTR model is specifically designed to be an attractive alternative to ownership without providing its benefits. Understanding that framing is the first step to not getting trapped in it indefinitely.

If you want to talk through what any of this means for your specific situation, whether you're thinking about selling, buying, or just trying to understand what's happening to this market, that's exactly what I'm here for.

- Two institutional deals totaling $212 million closed in Will County and Orland Park in the first 60 days of 2026, both acquiring large rental communities designed never to be sold to individual buyers.

- Build-to-Rent was a Sunbelt story for years. It's now expanding into Midwest suburbs, driven by tight supply and the fact that Chicago led the country in apartment rent growth in early 2026.

- The BTR model is built on the affordability gap, the growing number of households priced out of ownership who will rent single-family style homes indefinitely.

- Private equity is simultaneously consolidating the trades (HVAC, plumbing, electrical), HOA management, and water utilities, capturing not just housing but every financial layer of residential life.

- For current homeowners, equity is real, meaningful, and worth protecting. The gap between what ownership builds and what renting builds is wider than it has been in decades.

- This is not a neutral development. It deserves attention, informed opinion, and, at a policy level, a serious response.

Disclaimer: The information in this article is for educational and informational purposes only and does not constitute financial, legal, or investment advice. Deal data is sourced from CoStar News, Crain's Chicago Business, and public press releases; all figures are as reported at time of publication. Opinions expressed are those of the author. Raymond Kennedy is a licensed real estate broker in Illinois with eXp Realty.